Predictive analysis of NVIDIA CORP stock prices using machine learning techniques

Article Sidebar

Main Article Content

Abstract

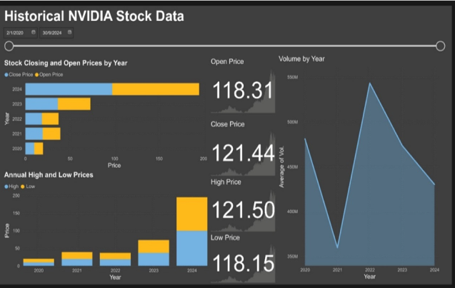

This research investigates the application of machine learning techniques to forecast NVIDIA Corporation's stock prices utilizing historical data from January 2020 to September 2024. The study consist of four models of machine learning (ML), which are Linear Regression, Support Vector Machine (SVM), Random Forest, and Gradient Boosting Machine (GBM). The models are primarily assessed based on regression metrics which are on their Mean Squared Error (MSE) and R² Score. In addition, classification metrics such as Accuracy and F1-score are considered in this study. The results indicate that the Random Forest and Gradient Boosting Machine models surpass the others, providing high accuracy and reliability in stock price prediction. The research has discussed the limitations of the study, including the dataset's scope and the exclusion of macroeconomic indicators. Recommendations for future research include expanding the dataset with longer time frames, incorporating additional features, and exploring advanced ML techniques. The result points out the significance of ML to financial forecasting, and it has big implications for investors and financial professionals.

Article Details

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

References

Alabi, O., & Bukola, T. (2023). Introduction to descriptive statistics. In IntechOpen eBooks. https://doi.org/10.5772/intechopen.1002475

Altork, Y. (2025). Comparative analysis of machine learning models for wind speed forecasting: Support vector machines, fine tree, and linear regression approaches. International Journal of Thermofluids, 27, Article 101217. https://doi.org/10.1016/j.ijft.2025.101217

Bollerslev, T. (1986). Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics, 31(3), 307-327. https://doi.org/10.1016/0304-4076(86)90063-1

Chen, X., Cao, L., Cao, Z., & Zhang, H. (2024). A multi-feature stock price prediction model based on multi-feature calculation, LASSO feature selection, and Ca LSTM network. Connection Science, 36(1), Article 2286188. https://doi.org/10.1080/09540091.2023.2286188

Chicco, D., & Jurman, G. (2020). The advantages of the Matthews correlation coefficient (MCC) over F1 score and accuracy in binary classification evaluation. BMC Genomics, 21(1). https://doi.org/10.1186/s12864-019-6413-7

Chicco, D., Warrens, M. J., & Jurman, G. (2021). The coefficient of determination R squared is more informative than SMAPE, MAE, MAPE, MSE, and RMSE in regression analysis evaluation. PeerJ Computer Science, 7, Article e623. https://doi.org/10.7717/peerj-cs.623

Cousineau, D., & Chartier, S. (2010). Outliers detection and treatment: A review. International Journal of Psychological Research, 3(1), 58-67. https://doi.org/10.21500/20112084.844

Heymans, M. W., & Twisk, J. W. (2022). Handling missing data in clinical research. Journal of Clinical Epidemiology, 151, 185-188. https://doi.org/10.1016/j.jclinepi.2022.08.016

Hodson, T. O., Over, T. M., & Foks, S. S. (2021). Mean squared error, deconstructed. Journal of Advances in Modeling Earth Systems, 13(12). https://doi.org/10.1029/2021MS002681

Huang, F. (2019). Data cleansing. In Springer eBooks (pp. 1-4). https://doi.org/10.1007/978-3-319-32001-4_300-1

Kumbure, M. M., Lohrmann, C., Luukka, P., & Porras, J. (2022). Machine learning techniques and data for stock market forecasting: A literature review. Expert Systems with Applications, 197, Article 116659. https://doi.org/10.1016/j.eswa.2022.116659

Mohammed, B., & Hamza, C. A. (2025). Robust estimation of blasting-induced flyrock using machine learning decision tree algorithms: Random Forest, Gradient Boosting Machine, and XGBoost. Mining, Metallurgy & Exploration, 42, 1609-1624. https://doi.org/10.1007/s42461-025-01267-4

Nelson, D. M., Pereira, A. C., & de Oliveira, R. A. (2017). Stock market's price movement prediction with LSTM neural networks. In Proceedings of the 2017 International Joint Conference on Neural Networks (IJCNN).

Pedregosa, F., Varoquaux, G., Gramfort, A., Michel, V., Thirion, B., Grisel, O., Blondel, M., Prettenhofer, P., Weiss, R., Dubourg, V., Vanderplas, J., Passos, A., Cournapeau, D., Brucher, M., Perrot, M., & Duchesnay, E. (2011). Scikit learn: Machine learning in Python. Journal of Machine Learning Research, 12, 2825-2830.

Phuoc, T., Anh, P. T. K., Tam, P. H., & Nguyen, C. V. (2024). Applying machine learning algorithms to predict the stock price trend in the stock market: The case of Vietnam. Humanities and Social Sciences Communications, 11(1), Article 393. https://doi.org/10.1057/s41599-024-02807-x

Sabri, M. F., Anthony, M., Law, S. H., Rahim, H. A., Burhan, N. A. S., & Ithnin, M. (2023). Impact of financial behaviour on financial well-being: Evidence among young adults in Malaysia. Journal of Financial Services Marketing, 29(3), 788-807. https://doi.org/10.1057/s41264-023-00234-8

Sonkavde, G., Dharrao, D. S., Bongale, A. M., Deokate, S. T., Doreswamy, D., & Bhat, S. K. (2023). Forecasting stock market prices using machine learning and deep learning models: A systematic review, performance analysis, and discussion of implications. International Journal of Financial Studies, 11(3), Article 94. https://doi.org/10.3390/ijfs11030094

The pandas development team. (2020). pandas (Version latest) [Computer software]. Zenodo. https://doi.org/10.5281/zenodo.3509134

Trinh, H. H., Nguyen, C. P., Hao, W., & Wongchoti, U. (2021). Does stock liquidity affect bankruptcy risk? DID analysis from Vietnam. Pacific Basin Finance Journal, 69, Article 101634. https://doi.org/10.1016/j.pacfin.2021.101634

Vujovic, Z. D. (2021). Classification model evaluation metrics. International Journal of Advanced Computer Science and Applications, 12(6), 599-606. https://doi.org/10.14569/ijacsa.2021.0120670